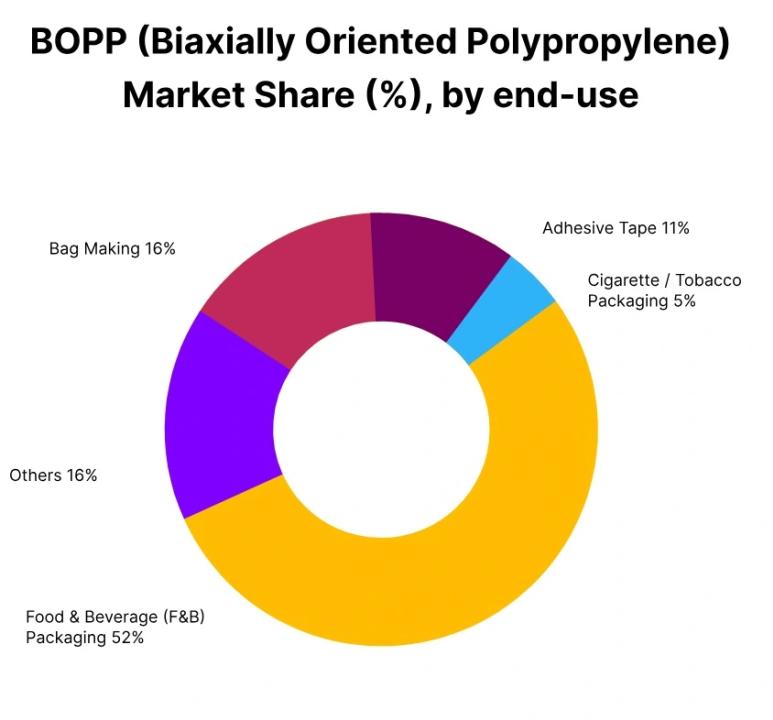

In Q3 2025, the overall global BOPP market showed a slight decline of around 1% compared to Q2 2025. This decline was mainly due to weak demand from packaging converters and limited export activity, especially across major Asian markets. Buyers across regions remained cautious, placing orders only when necessary and avoiding aggressive restocking. This conservative buying approach played a key role in shaping the BOPP Film Price Trend throughout the quarter.

Global Market Conditions and Demand Sentiment

One of the most noticeable features of the BOPP Film Price Trend in Q3 2025 was the lack of strong demand momentum. Many downstream buyers adopted careful procurement strategies, driven by uncertain order visibility and competitive pricing in the market. Packaging converters, in particular, focused on managing inventories rather than expanding purchases.

Feedstock polypropylene (PP) prices stayed largely stable during the quarter. While this stability helped prevent sharp cost increases for film producers, it also meant there was little upward cost pressure to support higher BOPP prices. As a result, film producers adjusted operating rates at several plants to avoid excess inventory buildup.

Export activity remained subdued across many regions. With ample supply available and pricing competition increasing, overseas buyers hesitated to place large orders. This situation added further pressure to the BOPP Film Price Trend, keeping it mostly flat to slightly bearish in several markets.

India: Strong Quarterly Gains with Late-Quarter Softening

India stood out as a relatively stronger market during Q3 2025. Domestically traded BOPP Film prices in Nashik averaged around USD 1,634 per metric ton, reflecting an 8% increase compared to Q2 2025. The BOPP Film Price Trend in India was supported by improved buying interest from downstream converters.

Consumption from food packaging, label stock, and lamination segments remained healthy throughout most of the quarter. Producers followed disciplined production plans, ensuring inventories stayed balanced despite improving demand. Feedstock PP prices remained range-bound, offering neutral cost support to manufacturers.

Export interest from Southeast Asia and the Middle East appeared intermittently, adding modest support. However, in September 2025, Indian BOPP prices saw a month-on-month decline of around 4%, driven by cautious restocking and competitive offers. Despite this, overall sentiment remained mildly optimistic.

China: Slight Decline in a Balanced Market

In China, the BOPP Film Price Trend showed a marginal decline of around 1% during Q3 2025. The market remained largely balanced, with stable but cautious trading conditions. Demand from food packaging, label films, and lamination applications stayed moderate, as buyers avoided aggressive purchasing.

Stable PP feedstock costs and controlled operating rates among major producers kept the market from swinging sharply in either direction. Expectations of stronger seasonal demand after holidays did not fully materialize, keeping sentiment neutral to slightly bearish.

In September, prices recorded a small month-on-month increase of nearly 1%, influenced by domestic price adjustments and controlled inventory levels. Overall, China’s market reflected stability with limited upward momentum.

United States: Gradual Softening Continues

The BOPP Film Price Trend in the United States recorded a modest 1% decline during Q3 2025, continuing the soft trend seen in late Q2. Prices remained within a narrow range as supply and demand stayed mostly balanced.

Demand from food packaging, labels, and industrial lamination remained moderate. Many converters continued conservative procurement, supported by sufficient inventory levels and availability of competitively priced imports. Stable PP feedstock prices and steady operating rates prevented sharp market movements.

In September, prices declined by another 1%, influenced by ongoing inventory adjustments and subdued trading activity. Market sentiment remained cautious as stronger consumer packaging demand did not fully emerge.

Mexico: Stable Supply, Mild Price Pressure

In Mexico, the BOPP Film Price Trend declined by around 1% during Q3 2025. The market continued to experience soft pricing conditions, similar to those seen toward the end of the previous quarter.

Demand from food packaging, adhesive labels, and lamination remained steady but unexciting. Converters maintained cautious buying habits, supported by stable inventories and competitive import options. Stable PP feedstock costs and consistent production levels kept supply balanced.

September saw another small month-on-month decline of around 1%, driven by slower procurement and subdued market activity.

Kenya: Strong Quarterly Gains Despite Late Dip

Kenya experienced a notable upward movement in the BOPP Film Price Trend, with prices rising by approximately 16% during Q3 2025. This marked a reversal from the softer conditions seen earlier.

Tighter supply, delayed import arrivals, and steady demand from food packaging and industrial laminates supported the market. Buyers remained active, especially as imports from Asia and the Middle East faced logistical delays.

Stable-to-firm PP feedstock costs and moderate operating rates further strengthened prices. However, in September, prices declined by around 4% as inventories eased and competitive offers returned to the market.

Nigeria: Firm Market with End-Quarter Correction

Nigeria also recorded a positive quarterly trend, with BOPP Film prices increasing by around 6% in Q3 2025. Demand from FMCG-related packaging, labels, and laminates remained healthy, supporting active procurement.

Supply constraints due to import delays contributed to firmer pricing. However, in September, prices dropped by about 5% as inventory tightness eased and buying slowed after earlier stocking.

Vietnam: Mostly Stable with Slight Decline

In Vietnam, the BOPP Film Price Trend showed minimal movement, declining by just 0.5% during Q3 2025. Balanced supply and consistent production kept prices stable.

Demand from food packaging and labels remained moderate, while buyers maintained cautious procurement strategies. September saw a further 1% decline, driven by competitive import offers and softer buying interest.

Malaysia: Mild Improvement with Stable Outlook

Malaysia recorded a slight 0.5% increase in Q3 2025, reflecting a stable market environment. Demand from packaging and FMCG sectors remained controlled but healthy, supporting mild price improvement.

However, September prices declined by around 1% due to competitive imports and easing inventories. Overall sentiment stayed cautiously optimistic.

Overall Market Outlook

Overall, the BOPP Film Price Trend in Q3 2025 reflected a market shaped by cautious demand, stable feedstock costs, and disciplined production. While most regions saw soft or stable pricing, select markets such as India, Kenya, and Nigeria showed stronger performance.

Looking ahead, the market’s direction will depend on improvements in packaging demand, export activity, and consumer spending. Until then, the BOPP film market is likely to remain balanced, with pricing movements closely tied to regional supply and demand dynamics.

Please Submit Your Query For BOPP Film Price Trend, Market Analysis and Forecast: https://www.price-watch.ai/book-a-demo/