The global virtual training and simulation market is transforming how industries train and upskill their workforce, leveraging immersive digital environments to boost efficiency, safety, and learning effectiveness. Driven by technological advancements and increasing demand for cost-effective training worldwide, the market reflects significant growth potential across sectors like healthcare, defense, aviation, and education.

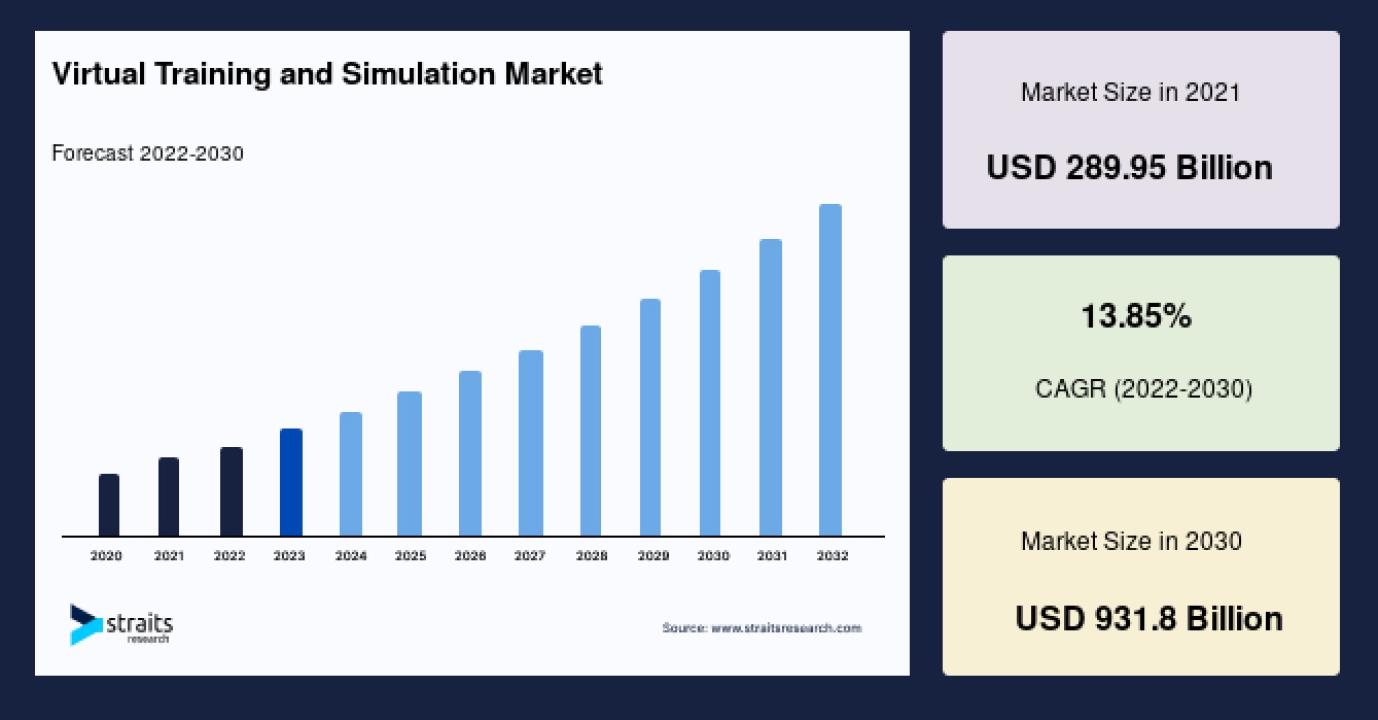

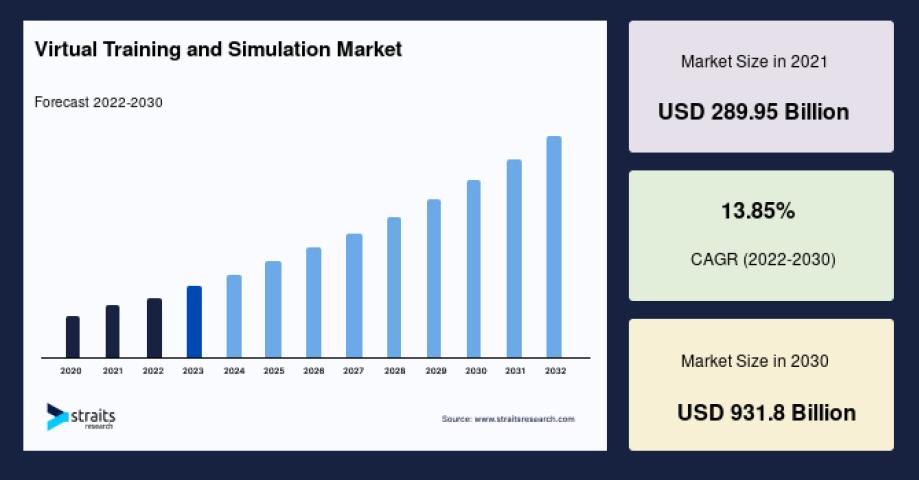

Market Size 2021 – USD 289.95 billion

Market Size 2030 – USD 931.8 billion

CAGR (2022-2030) – 13.85%

For detailed market data and free sample, download here: Request Sample – https://straitsresearch.com/report/virtual-training-and-simulation-market/request-sample

Market Drivers

Virtual training and simulation reduce the cost and risk of traditional hands-on training, especially in high-stakes fields such as aviation, healthcare, and defense. They allow trainees to practice complex, dangerous, or expensive procedures safely within controlled virtual environments. Increasing adoption of advanced technologies like augmented reality (AR), virtual reality (VR), and mixed reality (MR) has enhanced realism and engagement. The COVID-19 pandemic accelerated demand as organizations shifted to remote and decentralized learning models. Additionally, regulatory bodies are starting to mandate competency assessments via simulation for safety-critical roles, further boosting market adoption.

Market Challenges

Despite promising growth, cost remains a significant barrier, especially for small and medium enterprises. High development and implementation expenses, including hardware and software investments, create budgetary challenges. Integrating virtual training with legacy systems and ensuring user acceptance also require strategic change management. Another challenge is the need for content customization to meet diverse industry requirements, which demands skilled content creators and continuous updates. Cybersecurity and data privacy concerns related to cloud-based training platforms also warrant attention.

Market Segmentation

By Component

Hardware: This segment includes VR headsets, simulators, sensors, gloves, and other physical devices essential for immersive experiences. It currently holds the largest market share due to critical infrastructure needs.

Software: Encompasses training platforms, simulation software, content creation tools, and learning management systems (LMS). It is growing rapidly as demand increases for scalable and customizable solutions.

By End-User

Defense & Security: The largest segment, leveraging simulation for combat training, situational awareness, and equipment handling without battlefield risks.

Aviation: Flight simulators are widely used for pilot training, meeting regulatory requirements and improving safety.

Healthcare: Medical simulation enables skill training in surgeries, diagnostics, and emergency response.

Education: Increasing adoption in schools and universities for STEM subjects and vocational training.

Others: Manufacturing, automotive, oil and gas, and entertainment sectors also increasingly use virtual training for improved workforce readiness.

By Region

North America: Holds the largest market share, buoyed by early technology adoption, strong R&D capabilities, and regulatory mandates.

Asia-Pacific: Fastest-growing region due to rapid digitalization, government initiatives in education and defense, and expanding infrastructure.

Europe: Robust market presence with a focus on healthcare and aviation sectors.

LAMEA: Emerging market with growing interest in simulation-based training.

To purchase the full report: Buy Now this report – https://straitsresearch.com/buy-now/virtual-training-and-simulation-market

Top Players Analysis

Leading companies noted in Straits Research’s report bring diverse technology innovations and sector expertise:

CAE Inc. – Global leader offering flight simulators, healthcare training systems, and defense solutions.

Rheinmetall AG – Known for military simulators and tactical training platforms.

Raytheon Technologies Corporation – Provides advanced aerospace and defense simulation solutions.

Northrop Grumman Corporation – Specializes in defense and security training simulators.

Cubic Corporation – Offers IT-based simulation and training services.

Lockheed Martin – Supplies cutting-edge defense and aviation training simulators.

L3Harris Technologies – Develops virtual reality training systems for government and commercial use.

Thales Group – Focused on aerospace and defense training simulation.

Textron Inc. – Provides a range of simulation and training products, notably in aviation.

Honeywell International Inc. – Supplies industrial and aviation-related virtual training technologies.

These companies compete through innovation, partnerships, and strategic acquisitions to expand global footprints and address diverse industry needs.

Conclusion and About Us

The virtual training and simulation market is poised for dynamic growth influenced by evolving technological capabilities and increased emphasis on workforce readiness and safety. While challenges such as cost and integration persist, organizations worldwide increasingly recognize the long-term benefits of immersive training. North America leads in market size, but Asia-Pacific’s rapid growth signals broad global adoption. The market transformation promises improved skill acquisition, operational efficiency, and safety across sectors for years to come.

Straits Research is a market intelligence company providing global business information reports and services. Our exclusive blend of quantitative forecasting and trends analysis provides forward-looking insight for thousands of decision-makers. Straits Research Pvt. Ltd. provides actionable market research data, especially designed and presented for decision making and ROI.

FAQs

What is the global virtual training and simulation market size in 2021?

USD 289.95 billion.

What is the expected market size by 2030?

USD 931.8 billion.

What is the CAGR during 2022-2030?

13.85%.

Which component segment holds the largest market share?

Hardware, including VR headsets and simulators.

Which end-user industry dominates the market?

Defense and security sector.

What are the main drivers of virtual training market growth?

Cost-effectiveness, risk mitigation during training, technology adoption, and remote learning demands.

What are key challenges confronting the market?

High upfront costs, content customization needs, integration complexity, and cybersecurity concerns.