The global automotive refrigerant market has experienced significant growth due to rising demand for automotive air conditioning systems, increased vehicle production, and stringent government regulations focusing on reducing greenhouse gas emissions. Automotive refrigerants are crucial components in air conditioning units for vehicles, enhancing passenger comfort and safety. The market is driven by developments in refrigerant technology aimed at environmental sustainability, along with an increasing emphasis on energy efficiency and vehicle electrification.

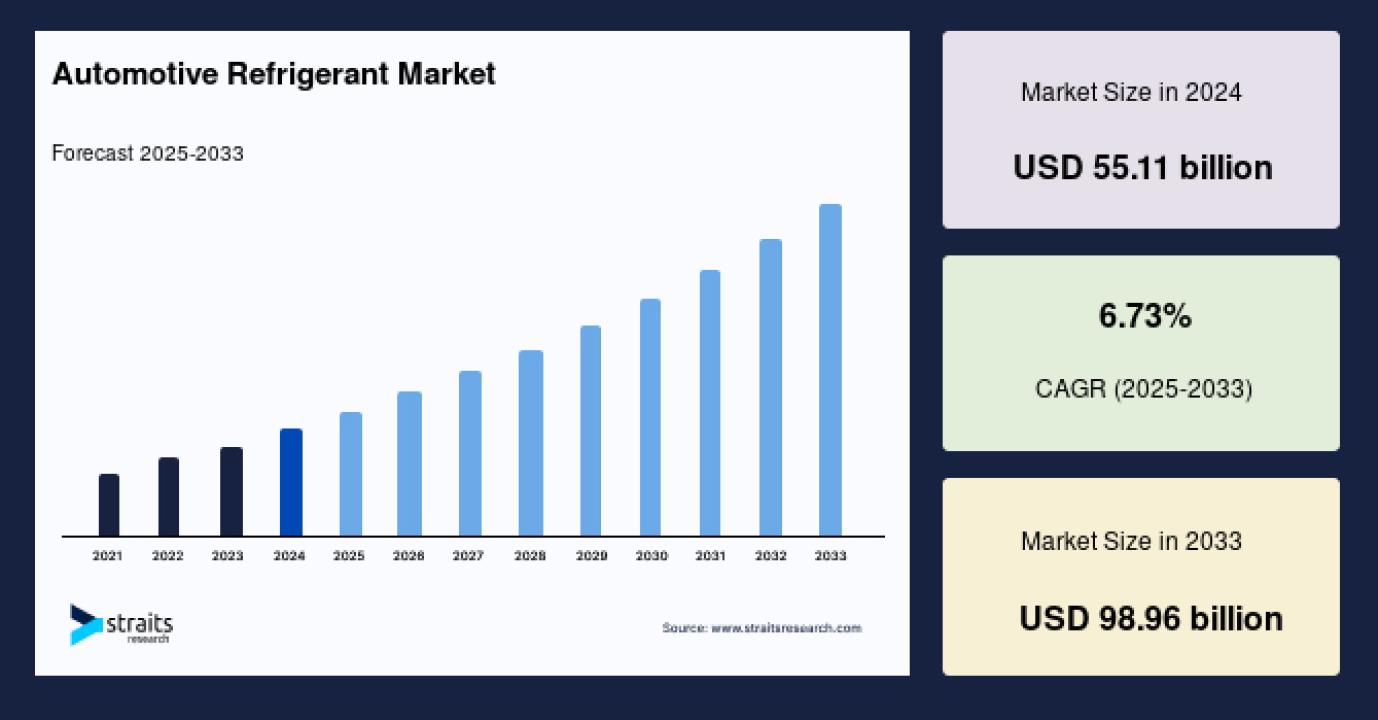

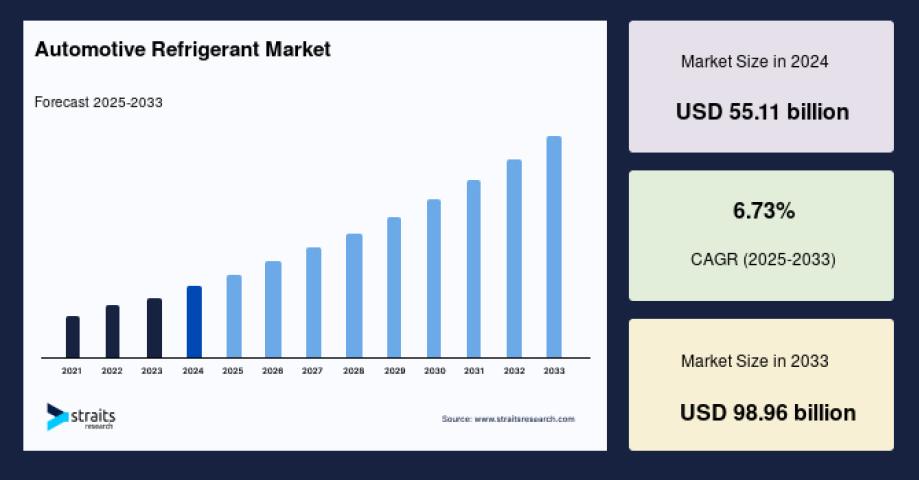

Market Size 2024 – USD 55.11 billion

Market Size 2025 – USD 58.81 billion

Market Size 2033 – USD 98.96 billion

CAGR (2025–2033) – 6.73%

📌 Request Sample - https://straitsresearch.com/report/automotive-refrigerant-market/request-sample

Market Drivers

The automotive refrigerant market is primarily driven by increasing automotive production worldwide, especially in emerging economies where vehicle ownership is rising rapidly. Heat management and passenger comfort continue to be critical factors pushing demand for efficient automotive air conditioning systems. Moreover, governments globally are imposing strict environmental regulations to reduce carbon emissions and phase out refrigerants with high global warming potential (GWP), prompting the adoption of eco-friendly alternatives such as hydrofluoroolefins (HFOs) and natural refrigerants.

Market Challenges

Despite strong demand, the automotive refrigerant market faces several challenges. The high cost of advanced refrigerants and continuous regulatory changes create a barrier for market participants. Compliance with international protocols such as the Kigali Amendment to the Montreal Protocol necessitates costly reformulations and shifts in supply chain logistics. Moreover, the flammability and toxicity concerns associated with some newer refrigerant types require rigorous safety standards, limiting their fast-track adoption.

Competition from alternative cooling technologies, such as adsorption cooling systems, could also hamper traditional refrigerant use. Finally, aftermarket service challenges concerning refrigerant refills and leak management add to operational complexities.

Market Segmentation

The automotive refrigerant market can be segmented by refrigerant type, vehicle type, and application.

By Refrigerant Type

- Hydrofluorocarbon (HFCs): Once dominant, HFC refrigerants like R-134a are being gradually phased down due to high GWP and environmental regulations.

- Hydrofluoroolefins (HFOs): Emerging as an eco-friendly alternative, HFOs such as R-1234yf offer low GWP and enhanced energy efficiency, gaining widespread acceptance in new vehicles.

- Natural Refrigerants: Includes CO2 (R-744) and hydrocarbons (propane, butane), valued for zero ozone depletion and low carbon footprint but challenged by safety and flammability concerns.

- Hydrochlorofluorocarbon (HCFCs): Older generation refrigerants with ozone-depleting potential are mostly banned or restricted in various regions.

By Vehicle Type

- Passenger Cars: The largest segment, driven by the continuous growth of passenger vehicle ownership and demand for comfortable driving environments.

- Commercial Vehicles: Includes buses, trucks, and vans; growth influenced by logistics and freight industry expansion.

- Electric Vehicles (EVs): A rapidly growing segment requiring specialized refrigerants designed for battery and cabin thermal management.

By Application

- Air Conditioning: Primary application encompassing passenger comfort systems in both new and existing vehicles.

- Refrigeration: Used in refrigerated transport vehicles for perishable goods.

- Others: Includes heat pumps and specialized cooling systems in automotive manufacturing.

Top Players Analysis

The automotive refrigerant market is highly competitive, with several key players driving innovation and growth globally:

- The Chemours Company: A leader known for its Chemours Opteon™ HFO refrigerants, supplying low-GWP alternatives globally.

- Honeywell International Inc.: Offers Solstice® branded refrigerants with advanced environmental profiles and extensive adoption in automotive OEMs.

- Arkema S.A.: Key provider of refrigerants including R-1234yf, focusing on sustainable products.

- Daikin Industries Ltd.: Offers innovative refrigerants as part of its HVAC product portfolio.

- Mitsubishi Chemical Corporation: Develops advanced hydrofluoroolefin refrigerants targeting automotive applications.

- Linde plc: Supplies industrial gases and refrigerants, supporting automotive manufacturers worldwide.

- Dongyue Group: A prominent Chinese manufacturer specializing in HFCs and transitioning to HFOs.

- SRF Limited: Provides a wide range of refrigerants, including eco-friendly HFOs for automotive sectors.

- Hubei Xingfa Chemicals Group Co., Ltd.: Supplier focused on both domestic and international refrigerant markets.

- Sinochem Group: Engaged in the production of specialty chemicals and refrigerants with growing automotive refrigerant offerings.

These companies emphasize R&D and partnerships with automakers to comply with evolving regulations and meet consumer demand for greener refrigerant solutions.

📌 Buy Now this report - https://straitsresearch.com/buy-now/automotive-refrigerant-market

Conclusion

The automotive refrigerant market is positioned for robust growth fueled by rising vehicle production, increased regulatory pressures to phase out high-GWP substances, and rising adoption of electric vehicles requiring advanced thermal management. Challenges such as regulatory compliance and safety concerns remain but prompt continuous innovation. Market participants actively invest in developing low-GWP, energy-efficient refrigerants, making this an evolving and dynamic industry.

Straits Research is a market intelligence company providing global business information reports and services. Our exclusive blend of quantitative forecasting and trends analysis provides forward-looking insight for thousands of decision-makers. Straits Research Pvt. Ltd. provides actionable market research data, especially designed and presented for decision making and ROI.