Buying a new car is an exciting

milestone, but protecting it with the right insurance coverage is equally

important. While a comprehensive car insurance policy offers essential

protection, it may not cover certain real-world risks such as depreciation

loss, engine damage due to water ingress, roadside breakdowns, or total loss

situations.

This is where add-on covers in car

insurance become extremely valuable.

In this detailed guide, we will

explain the most important add-on covers for new car insurance, how they work,

who should opt for them, and how they enhance your financial security.

What

Are Add-On Covers in Car Insurance?

Add-ons (also called riders) are

optional benefits that enhance your base comprehensive car insurance policy.

They provide extended coverage against risks that are not included in a

standard plan.

A comprehensive policy typically

covers:

- Own damage

- Third-party liability (mandatory under the Motor

Vehicles Act)

- Fire, theft, and natural calamities

However, it does not cover

depreciation deductions, engine damage due to flooding, roadside assistance, or

consumables—unless you purchase specific add-ons.

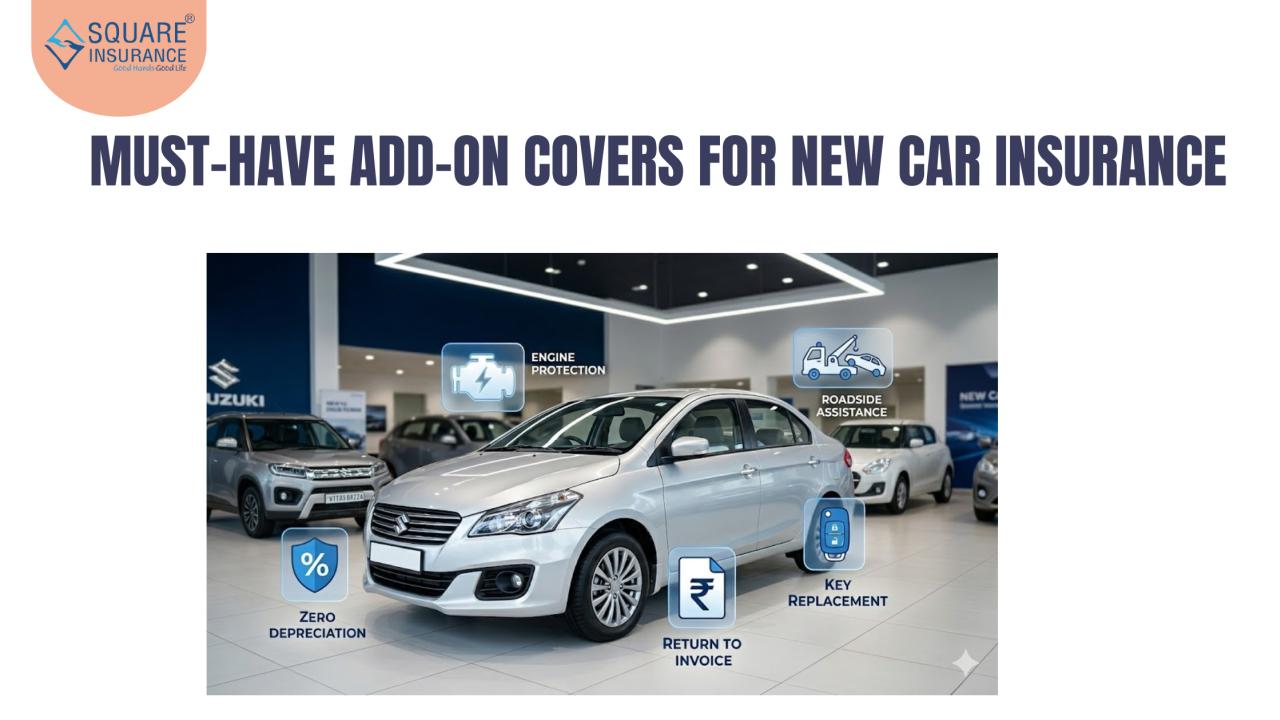

1. Zero Depreciation Cover (Nil Dep Cover)

New vehicles depreciate quickly.

During a claim, insurers deduct depreciation on replaced parts such as plastic,

rubber, and metal components.

With Zero Depreciation Cover:

- No deduction on replaced parts

- Higher claim settlement amount

- Minimal out-of-pocket expenses

Ideal

For:

- Brand-new cars

- Luxury vehicles

- Cars with expensive spare parts

For the first 3–5 years of

ownership, this add-on is highly recommended.

2. Engine Protection Cover

Standard policies do not cover

engine damage caused by:

- Water ingress during floods

- Oil leakage

- Hydrostatic lock

Engine repair costs can be extremely

high.

Engine Protection Cover includes:

- Repair or replacement of engine parts

- Gearbox damage

- Differential assembly damage

Ideal

For:

- Flood-prone areas

- Metro cities

- High-value vehicles

3. Return to Invoice (RTI) Cover

In case of total loss or theft,

insurers normally pay the Insured Declared Value (IDV), which is lower than the

original invoice value.

With RTI Cover:

- You receive the original invoice price

- Registration charges and road tax may be included

Ideal

For:

- New cars (within 3 years)

- Financed vehicles

- Expensive cars

This add-on protects you from major

financial loss in total damage situations.

4. No Claim Bonus (NCB) Protection Cover

If you do not make any claims during

the policy year, you earn a No Claim Bonus, which reduces renewal premiums.

However, one claim can reset your

accumulated bonus.

NCB Protection allows:

- One or two claims without losing your NCB

- Continued premium savings

Ideal

For:

- Safe drivers

- Long-term policyholders

5. Roadside Assistance (RSA) Cover

Unexpected breakdowns can happen

anytime.

RSA provides:

- Towing service

- Battery jump-start

- Flat tyre assistance

- Emergency fuel delivery

- Minor on-the-spot repairs

Ideal

For:

- Frequent highway drivers

- New drivers

- Family travelers

6. Consumables Cover

Standard insurance does not cover

consumable items like:

- Engine oil

- Coolant

- Brake oil

- Nuts and bolts

- Lubricants

Consumables Cover reimburses these

small but frequent expenses during claims.

Ideal

For:

- New car owners

- Frequent repair situations

7. Key Replacement Cover

Modern vehicles use smart keys and

electronic locking systems that are costly to replace.

This add-on covers:

- Lost or stolen keys

- Lock replacement

- Labor charges

Ideal

For:

- Cars with advanced key systems

- Premium vehicles

8. Tyre Protection Cover

Tyre damage due to cuts, bulges, or

bursts is usually not covered unless caused by an accident.

Tyre Protection includes:

- Sidewall damage

- Tyre burst

- Bulges

Ideal

For:

- SUVs

- High-performance vehicles

- Rough road usage

Do Add-Ons Increase Premium?

Yes, but the increase is relatively

small compared to potential repair expenses.

For example:

- Zero Dep may increase premium slightly

- Engine Protection adds moderate cost

- RSA is usually affordable

The financial protection offered

often outweighs the additional premium.

Priority Add-Ons for New Car Owners

If budget is limited, prioritize:

- Zero Depreciation Cover

- Engine Protection Cover

- Return to Invoice Cover

- Roadside Assistance

These provide maximum financial

value for new cars.

Conclusion

A new car deserves complete

protection beyond basic insurance coverage. While a comprehensive policy forms

the foundation, add-on covers such as Zero Depreciation, Engine Protection,

Return to Invoice, and Roadside Assistance significantly enhance financial

security.

Selecting the right add-ons ensures

that unexpected accidents, breakdowns, or total loss situations do not cause

major financial stress.

For expert assistance in choosing

the right add-ons tailored to your needs, Square Insurance can help you compare plans and select the most

suitable coverage for your new vehicle.

Frequently Asked Questions

1.

Are add-on covers compulsory for new cars?

No, they are optional but strongly

recommended for enhanced protection.

2.

Can I add riders later?

Yes, most insurers allow adding or

removing add-ons at renewal.

3.

Is Zero Depreciation necessary for new cars?

Yes, especially during the first few

years when depreciation deductions are high.

4.

How long is RTI cover available?

Typically for cars up to 3 years

old.

5.

Do add-ons work with third-party insurance?

No, add-ons are available only with

comprehensive car insurance.