There is a certain kind of startup founder who is meticulous about investor due diligence — who has their cap table in order, knows their unit economics cold, and would..

As CES 2026 approaches, technology is moving beyond futuristic gadgets toward practical, human-focused solutions The Las Vegas showcase highlights startups that bridge advanced engineering with everyday usability. This year’s theme..

Innovation often carries within it the seeds of its own disruption, and this paradox sits at the heart of The Innovator’s Dilemma, the seminal work by Clayton M. Christensen. Christensen..

Startups face unique banking needs: minimal fees, flexible access, strong tech integrations, and startup‐friendly credit or services. Choosing the right bank at the early stage can save time, money, and..

Startups often face significant challenges when trying to secure the capital needed to transform innovative ideas into scalable businesses. Traditional fundraising methods, such as pitching to venture capital firms or..

The mobile game market has developed into a multi-billion-dollar ecosystem that is changing how we are all engaging with games every day. Hyper casual puzzle games, multiplayer battle arenas, narrative-led..

Marketing is more than just promotion; it is the engine that drives sustainable business growth. Companies that master the art of understanding their customers, positioning their brand effectively, and communicating..

Every great company begins as a spark—an idea that ignites and refuses to fade. Today, the world is more fertile than ever for turning that spark into something extraordinary. Technology,..

Few things feel more personal than a small business. Built with effort, long nights, and often tight budgets, these ventures represent more than just commerce—they're trust in action. But behind..

Armed conflicts have always had profound consequences for the global economy. However, in today's interconnected world, wars have a much greater impact on businesses than in previous decades. Conflicts such..

Understanding market cycles is one of the most powerful tools available to investors seeking consistent long-term returns. Every economy moves through recognizable stages—expansion, peak, contraction, and recovery—and each phase presents..

Risk investment strategies are essential for startups and investors aiming to maximize returns in a highly competitive market. Venture capital and angel investing thrive on high-risk, high-reward opportunities, and understanding..

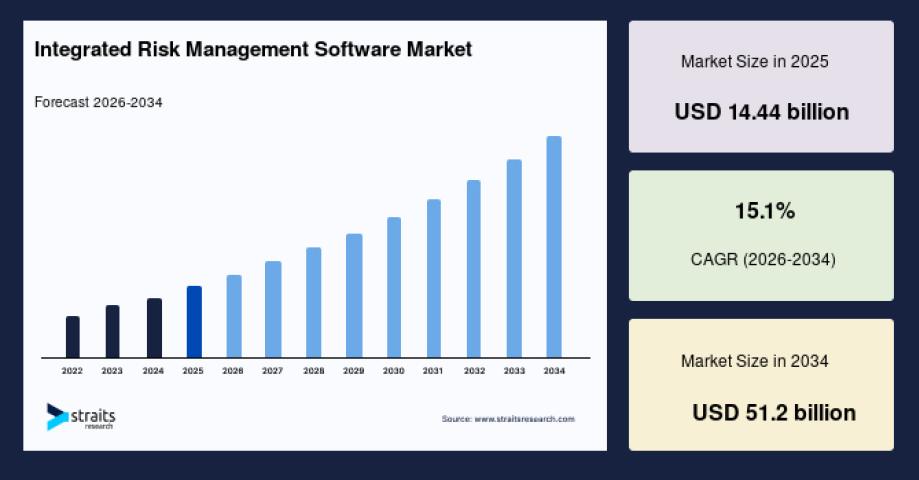

The global integrated risk management software market is witnessing significant growth due to increasing regulatory compliance requirements, rising cybersecurity threats, and growing adoption of enterprise-wide risk management strategies. The global..

The allure of Artificial Intelligence (AI) for large organizations is undeniable. From boosting efficiency to unlocking new revenue streams, AI-driven strategies promise transformative benefits. However, embarking on this journey is..

We help corporates, MNCs, and growing businesses identify, assess, and manage risks that may impact their operations, financial stability, and strategic objectives. Our Risk Management Services in India are designed..

Managing enterprise risks requires a systematic and data-driven approach. In the center of this strategy, grc risk management software enables organizations to identify, assess, monitor, and mitigate risks across departments...

The global business ecosystem is increasingly exposed to uncertainties, from financial risks and regulatory compliance to cyber threats and operational disruptions. In this environment, risk analytics has become an indispensable..

Skytree Scientific LRA Plus™ simplifies lightning risk management by turning a complex, multi-step process into a guided workflow that reduces friction from intake to final report. The platform centers on..