According to IMARC Group's report titled "India Copper Pipes and Tubes Market Size, Share, Trends and Forecast by Finish Type, Outer Diameter, End-User, and Region, 2026-2034", the report offers a comprehensive analysis of the industry, including market growth drivers, forecast, trends, share, and regional insights.

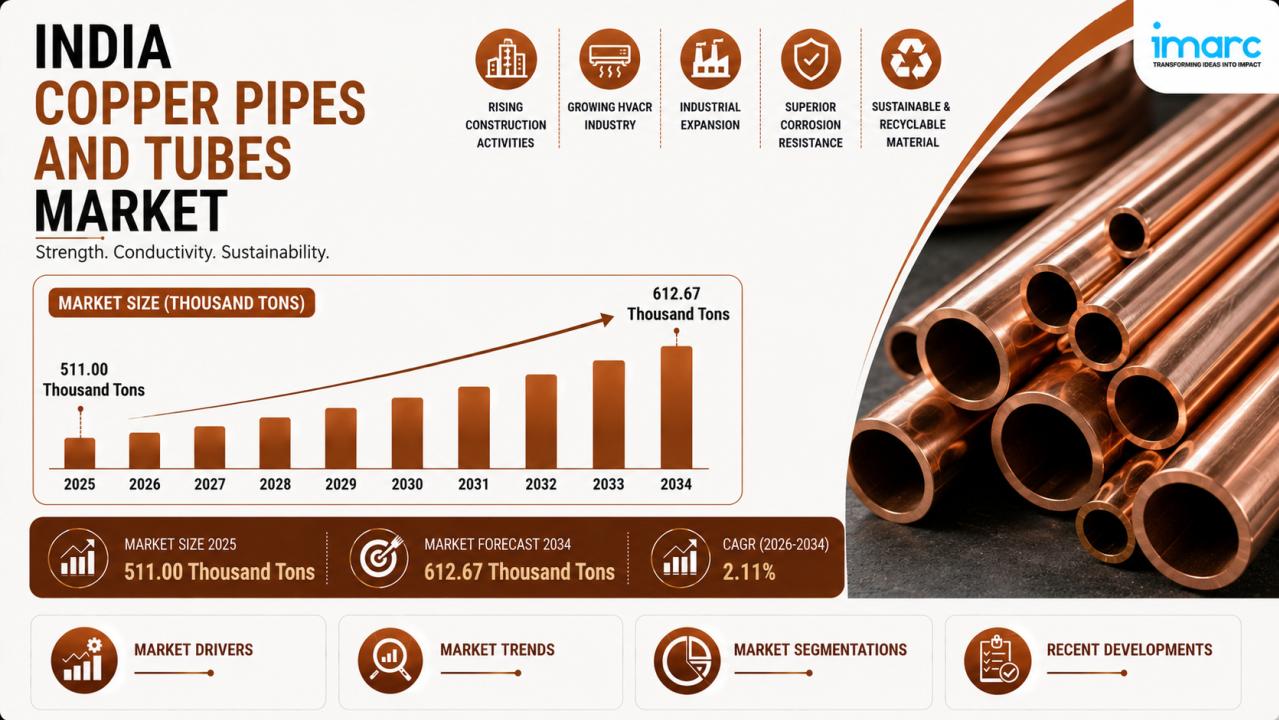

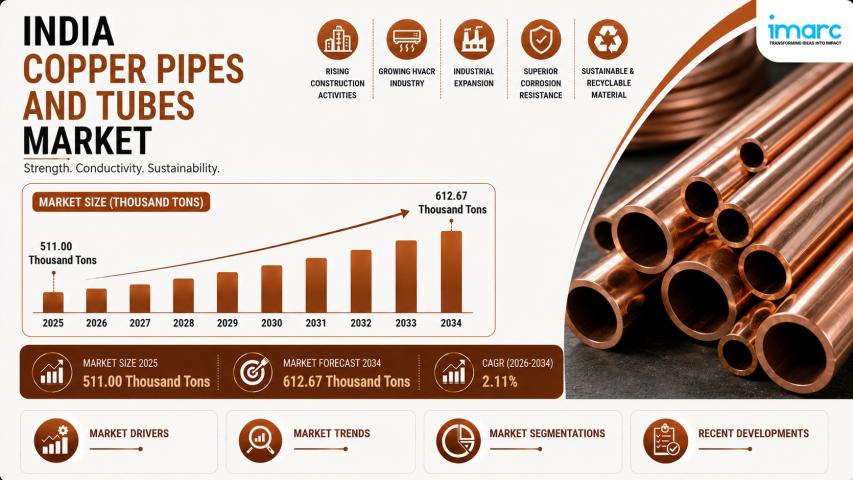

India's copper pipes and tubes market is growing steadily on the back of real, measurable drivers the market stood at 511.00 Thousand Tons in 2025 and is expected to reach 612.67 Thousand Tons by 2034, supported by expanding HVAC adoption, construction activity, and a domestic copper production base that is getting meaningfully stronger.

- The market is growing at a CAGR of 2.11% during 2026–2034 modest in percentage terms, but volume-significant given the scale of India's urbanization and infrastructure pipeline.

- LWC grooved copper tubes hold a 38.5% share by finish type in 2025, driven by their superior heat transfer efficiency and near-universal adoption in modern HVAC refrigeration systems.

- HVAC is the largest end-use segment at 41.5% in 2025 and India's HVAC market itself is projected to grow at a CAGR of 14.89% during 2026–2034, according to IMARC Group, creating a strong downstream pull for copper tubing.

- West India leads regionally with a 30.5% share, anchored by Maharashtra and Gujarat's concentration of manufacturing, commercial real estate, and HVAC-intensive industrial activity.

- Domestic capacity expansion including Adani's USD 1.2 Billion Mundra copper plant and Hindalco's INR 2,450 Crore Gujarat investment is gradually reducing India's dependence on imported refined copper and improving supply security for downstream tube manufacturers.

The Strategic Market Challenge: Navigating the Copper Pipes and Tubes Market in India

The most persistent structural challenge in this market is India's dependence on imported copper concentrates. Domestic ore reserves cover only a fraction of refinery requirements, which means that raw material availability and pricing for tube manufacturers is substantially exposed to global supply chain conditions, currency movements, and concentrate availability from major producing countries. This import dependency is not easily resolved in the short term even as domestic smelting capacity expands, the concentrate supply gap creates a structural cost and margin risk that runs through the entire value chain from smelter to finished tube manufacturer.

India's Strategic Vision for the Copper Pipes and Tubes Market:

- PM Awas Yojana Urban 2.0 creating direct downstream demand: The government's commitment of ₹10 Lakh Crore for housing construction targeting one crore urban families is generating sustained demand for copper piping in plumbing, water distribution, and HVAC systems across newly built residential units a demand signal that is large enough to underpin manufacturer capacity planning decisions over the medium term.

- Smart Cities Mission driving urban infrastructure copper consumption: Smart Cities Mission investments in urban utilities, public infrastructure, and institutional buildings are creating consistent demand for durable, high-performance piping materials a category where copper's corrosion resistance and service life credentials continue to justify its selection over polymer alternatives in quality-driven project specifications.

- Domestic copper production expansion improving supply chain resilience: Adani Group's USD 1.2 Billion Mundra copper plant adding 0.5 million tons per year of refined copper capacity in its first phase with a target of 1 million tons annually by FY29 represents a structural improvement in India's domestic raw material base that directly benefits downstream tube manufacturers seeking supply security and competitive cathode pricing.

- Circular economy and recycling infrastructure reducing import pressure: Hindalco Industries' INR 2,450 Crore investment in Gujarat including India's first copper and e-waste recycling plant at Dahej, designed to process 300–350 kilotons of scrap annually adds a meaningful secondary copper supply stream that improves overall feedstock availability and aligns with India's resource efficiency objectives.

➤ Access Industry-Focused Insights and Future Forecasts - Request Sample Report

Why Invest in the India Copper Pipes and Tubes Market: Key Growth Drivers & ROI

- HVAC sector expansion providing durable, high-volume demand: With HVAC holding 41.5% of copper tube end-use demand and India's HVAC market growing at a projected 14.89% CAGR, the demand pull from air conditioning and refrigeration manufacturers is structurally strong and multi-year in nature. As urban households, commercial buildings, hospitals, and cold storage facilities all expand HVAC adoption simultaneously, copper tube consumption in refrigerant circuit applications grows in lockstep creating predictable volume demand for manufacturers with reliable supply chains.

- Downstream capacity investment signaling manufacturer confidence: In 2024, Ram Ratna Wires approved an INR 200 Crore investment to expand its Bhiwadi plant with a dedicated DHP copper tube manufacturing line a commitment that reflects genuine demand visibility rather than speculative expansion. In July 2025, Adani Enterprises partnered with MetTube in a 50:50 structure across Kutch Copper Tubes Ltd. and MetTube Copper India Pvt. Ltd., combining Adani's Mundra copper infrastructure with MetTube's global manufacturing expertise specifically to serve HVAC, refrigeration, and plumbing demand.

- Construction scale creating sustained plumbing and building services demand: India's urbanization rate approximately 36.87% of the population in urban areas as of 2024 per World Bank data continues to drive residential and commercial construction at a pace that consistently absorbs copper piping for plumbing, water distribution, and building services. Large-scale projects like Shapoorji Pallonji's VANAHA Verdant residential development in Pune covering 5 acres with nearly 10 lakh square feet of saleable area illustrate the kind of project scale that generates meaningful copper tube demand per development.

- Quality and lifecycle efficiency driving copper preference over alternatives: Buyers across commercial, institutional, and industrial construction are increasingly evaluating piping materials on total lifecycle cost rather than upfront price alone. Copper's corrosion resistance, service longevity, and reliability in concealed installations where access for repair is limited support a strong performance-based procurement argument that is gaining traction among consultants, facility operators, and premium builders even as polymer alternatives compete on initial material cost.

India Copper Pipes and Tubes Market Trends & Future Outlook:

- The market is expected to reach 612.67 Thousand Tons by 2034 at a CAGR of 2.11%, according to IMARC Group steady volume growth reflecting the combined pull of housing construction, HVAC adoption, and industrial infrastructure expansion across India's urbanizing economy.

- LWC grooved tube dominance is set to strengthen further as India's HVAC market expands the segment's internal spiral groove structure improves heat transfer efficiency in refrigerant systems, making it the standard specification for OEMs producing split air conditioners and commercial cooling equipment.

- In October 2025, BIS Chennai organized a stakeholder review of the draft revised Indian standard for wrought copper tubes in refrigeration and air conditioning a signal that quality, energy efficiency, and sustainability standards for the sector are being actively updated to align with international benchmarks.

- Tier-II and Tier-III city expansion is becoming a more material demand driver as HVAC adoption spreads beyond metros and construction activity accelerates in secondary urban centers supported by government housing and infrastructure programs.

- Copper recycling infrastructure led by investments like Hindalco's Dahej facility is beginning to mature as a secondary supply source, improving feedstock availability for tube manufacturers and gradually reducing the sector's structural vulnerability to imported concentrate price swings.

Market Segmentation Breakdown and Share Analysis:

Analysis by Finish Type:

- LWC Grooved (High demand in ACs for better heat transfer)

- Straight Length (Preferred in plumbing and medical gas)

- Pancake

- LWC Plain

LWC grooved tubes dominate the market with a 38.5% share in 2025, driven by their compatibility with HVAC and refrigeration systems and widespread use in residential and commercial split air-conditioning installations.

Analysis by Outer Diameter:

- 3/8, 1/2, 5/8 Inch

- 3/4, 7/8, 1 Inch

- Above 1 Inch

The 3/8, ½, and 5/8 inch segment leads with a 45.5% market share in 2025, owing to its extensive adoption in air-conditioning and refrigeration equipment specified by OEMs.

Analysis by End-User:

- HVAC (Dominant segment due to AC and refrigeration manufacturing)

- Industrial Heat Exchanger

- Plumbing

- Electrical

- Others

HVAC accounts for 41.5% of the market in 2025, supported by the growing deployment of air-conditioning and refrigeration systems across residential, commercial, and industrial sectors.

Regional Insights:

- West India: Leading region, home to major copper refineries (Birla Copper, Adani) and downstream manufacturers.

- North India

- South India

- East India

West India holds a 30.5% share in 2025, driven by strong industrial manufacturing activity, expanding commercial real estate development, and high HVAC adoption in Maharashtra and Gujarat.

By the IMARC Group, the Top Competitive Landscape & their Positioning:

Covering an in-depth analysis of the competitive landscape, market structure, key player positioning, competitive dashboards, top winning strategies, and detailed profiles of all major industry participants you will gain access to all these exclusive insights within the full research report.

Note: If you need specific information that is not currently within the scope of the report, we can provide it to you as a part of the customization.

Regulatory Landscape & Policy Catalysts in India:

- PM Awas Yojana Urban 2.0 Ministry of Housing and Urban Affairs: With ₹10 Lakh Crore committed to housing construction for one crore urban families, PMAY-U 2.0 is the single largest policy driver of downstream copper tube demand in residential plumbing and HVAC applications creating a multi-year, government-backed construction pipeline that tube manufacturers can plan against with reasonable confidence.

- Smart Cities Mission Ministry of Housing and Urban Affairs: Smart Cities Mission funding for urban infrastructure development across 100 designated cities is generating consistent institutional demand for durable piping materials in public buildings, healthcare facilities, and urban utilities segments where copper's performance credentials support specification preference over lower-cost alternatives.

- Bureau of Indian Standards IS 10773 standard revision: BIS's active review of the Indian standard for wrought copper tubes used in refrigeration and air conditioning with the October 2025 stakeholder consultation covering quality, safety, energy efficiency, and sustainability is progressively raising the quality baseline for copper tube manufacturing and creating compliance-based differentiation opportunities for manufacturers investing in precision and certification.

- Plastic Waste Management Rules indirect copper demand support: FSSAI and MoEFCC regulations tightening plastic and polymer use in certain applications indirectly support copper's position as a preferred alternative in plumbing and building services particularly where regulatory preference for durable, recyclable materials aligns with copper's lifecycle credentials.

- Make in India for metals and manufacturing: Government emphasis on domestic manufacturing self-reliance across industrial sectors supports investment in copper tube production capacity as demonstrated by the Adani-MetTube partnership and Ram Ratna Wires' capacity expansion reducing India's dependence on imported finished copper tube products and strengthening the domestic supply chain.

- FDI policy for metals and manufacturing 100% automatic route: India's liberalized FDI framework for metals manufacturing enables international partnerships like the Adani-MetTube joint venture, facilitating technology transfer from global copper tube producers with established manufacturing expertise in precision HVAC-grade tubing into India's expanding domestic production base.

➤ Tailor the Research to Your Exact Business Needs - Request Customization

Frequently Asked Questions (FAQs):

Q1: What is the current size and projected growth of the India Copper Pipes and Tubes Market?

According to IMARC Group, the India Copper Pipes and Tubes Market reached 511.00 Thousand Tons in 2025 and is projected to reach 612.67 Thousand Tons by 2034, growing at a CAGR of 2.11% during 2026–2034. This growth is driven by expanding HVAC adoption, residential and commercial construction activity, and industrial infrastructure development across India's urbanizing economy.

Q2: Which finish type and outer diameter segment leads the market?

LWC grooved dominates by finish type with a 38.5% share in 2025, preferred for its superior internal heat transfer efficiency in HVAC refrigeration systems. By outer diameter, the 3/8, ½, and 5/8 inch segment leads with a 45.5% share reflecting these sizes' near-universal specification by air conditioner and refrigeration OEMs for refrigerant circuit applications in residential and commercial cooling systems.

Q3: Which end-use sector drives the most copper tube demand in India?

HVAC is the largest end-use segment with a 41.5% market share in 2025, followed by industrial heat exchange, plumbing, and electrical applications. The HVAC segment's dominance is reinforced by India's rapidly expanding air conditioning market projected to grow at a CAGR of 14.89% during 2026–2034 which creates consistent volume demand for copper tubes in refrigerant circuits across residential, commercial, and industrial cooling installations.

Q4: Which region leads the India Copper Pipes and Tubes Market and why?

West India leads with a 30.5% market share in 2025, anchored by Maharashtra and Gujarat's concentration of manufacturing clusters, commercial real estate development, and HVAC-intensive industrial activity. The region's major port infrastructure also supports efficient raw material import and finished product distribution a logistical advantage that reinforces its position as India's primary copper tube consumption and production hub.

Q5: What are the key challenges facing the India Copper Pipes and Tubes Market?

Three challenges stand out. Global copper price volatility driven by geopolitical conditions and demand from major consuming economies creates margin pressure and complicates procurement planning for tube manufacturers. Competition from CPVC, PVC, and cross-linked polyethylene alternatives in price-sensitive plumbing segments limits copper's addressable market in affordable housing and low-budget commercial construction. And India's structural import dependency for copper concentrates exposes the entire value chain to currency risk and supply disruption a constraint that domestic smelting expansion is gradually addressing but has not yet fully resolved.

Strategic Insight & Verdict

We at IMARC Group have observed that the India Copper Pipes and Tubes Market presents a straightforward, volume-driven investment case one grounded in the practical realities of urbanization, HVAC market expansion, and a domestic copper production base that is becoming more self-sufficient. Investors and manufacturers focused on HVAC-grade tube production, domestic raw material security, and distribution reach into tier-II and tier-III cities will be best positioned as the market moves from 511.00 Thousand Tons toward 612.67 Thousand Tons by 2034.

Source: India Copper Pipes and Tubes Market Report by IMARC Group