The global metro rail infrastructure market is witnessing robust expansion, propelled by rapid urbanization, population growth, and the demand for modern, sustainable transportation systems. As cities worldwide face mounting challenges of traffic congestion, carbon emissions, and limited mobility, metro rail networks are emerging as the backbone of urban mass transit solutions.

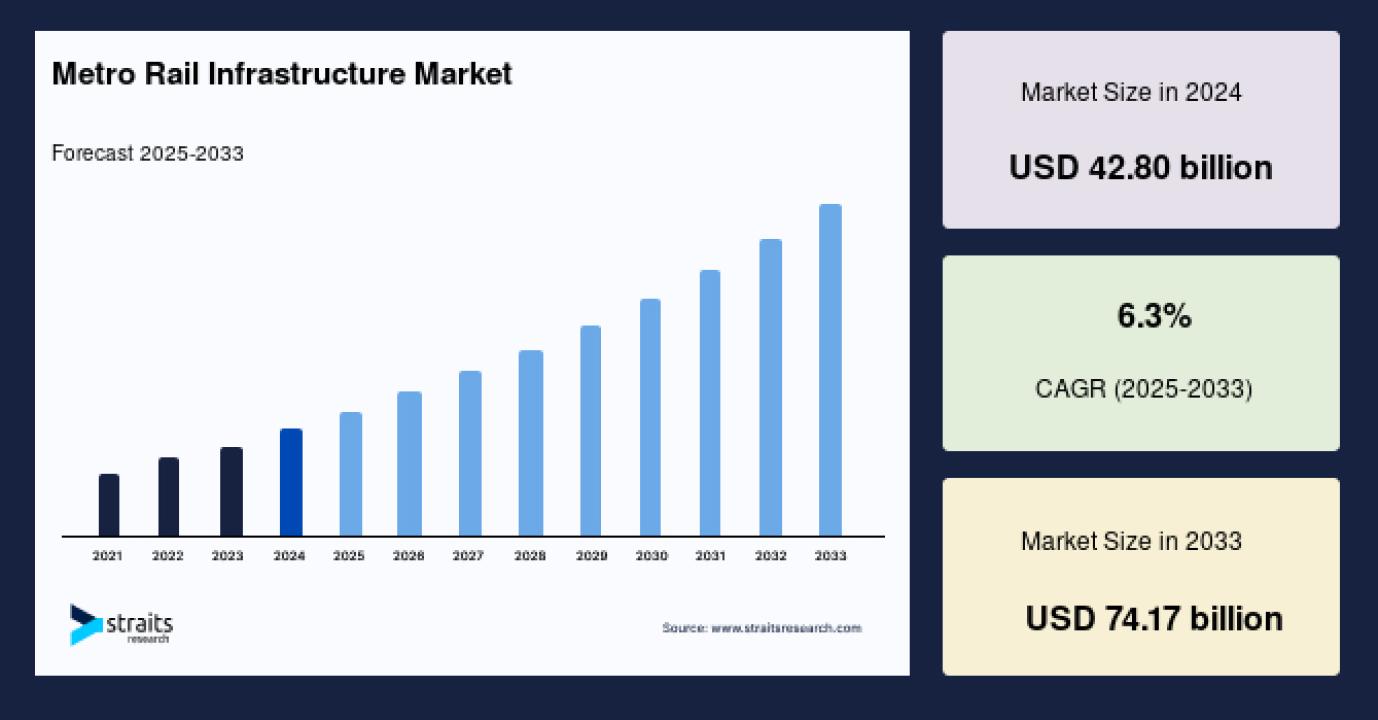

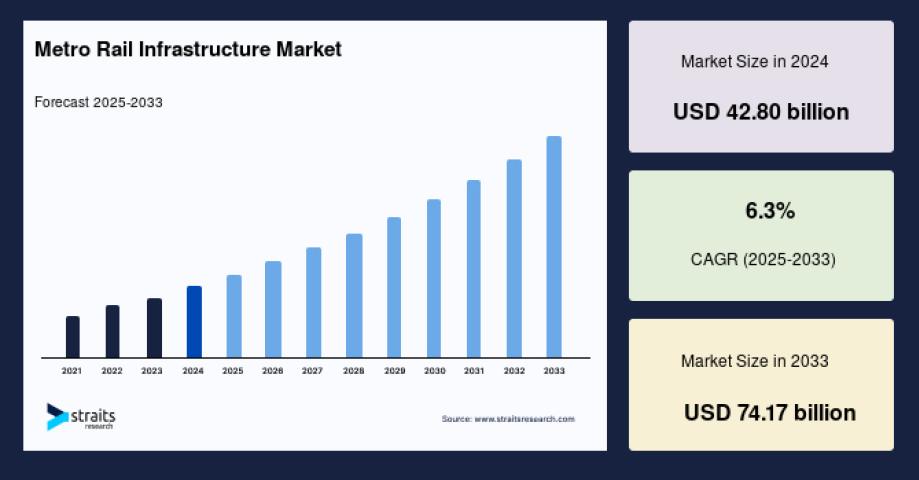

According to Straits Research, the market is projected to grow from USD 42.80 billion in 2024 to USD 74.17 billion by 2033, reflecting a CAGR of 6.3% (2025–2033).

📥 For detailed insights, segmentation, and regional analysis, download a free sample report here: Request Sample.

Market Overview

Metro rail infrastructure encompasses a wide range of systems, including trains, stations, tracks, signaling, communication, power supply, and maintenance facilities, all designed to provide fast, high-capacity transit in urban areas. By reducing traffic congestion, minimizing travel times, and lowering environmental impacts, metro systems serve as vital tools for sustainable urban development.

The UN projects an additional 2.5 billion people will move into cities by 2050, highlighting the critical need for metro rail as a cornerstone of future city planning.

Key Market Drivers

Several factors are fueling the market’s growth trajectory:

Urbanization & Migration: The surge of populations into megacities necessitates efficient, large-scale public transit solutions.

Government Initiatives: Programs like China’s Belt and Road Initiative (BRI) and India’s Smart Cities Mission prioritize metro expansions.

Environmental Concerns: Metro systems reduce greenhouse gas emissions and road congestion, supporting global sustainability goals.

Technological Innovations: Advancements such as driverless trains, smart ticketing, IoT-based monitoring, and automation are revolutionizing passenger experiences.

Public-Private Partnerships (PPPs): Collaborative models are accelerating infrastructure investments and execution.

Market Challenges

Despite its promising outlook, the market faces notable hurdles:

High Capital Requirements: Substantial upfront investments and long-term financing needs delay many projects.

Regulatory & Land Acquisition Issues: Securing approvals and land rights often slows construction.

Economic Uncertainty: Shifting political priorities can disrupt funding.

Environmental Concerns: Elevated metro structures bring challenges such as noise and visual impact mitigation.

Market Segmentation

By Metro Rail Type

Elevated Metro Rail: Fastest to build, cost-efficient, and dominant in global adoption.

Underground Metro Rail: Ideal for dense cities but more complex and expensive.

At-grade Metro Rail: Cost-effective but limited to less congested regions due to traffic interference.

By Component

Alignment & Trackwork – Fundamental for safety and train movement.

Station Building – Largest segment, driven by the need for accessibility, safety, and passenger amenities.

Signaling & Telecommunication – Crucial for operational safety and real-time management.

Rolling Stock – Includes trains and carriages essential for transport capacity.

Others – Power supply, maintenance depots, and real estate integration.

By Region

Asia-Pacific: Largest market, led by China, India, and Southeast Asia, supported by heavy infrastructure spending.

North America: Fastest-growing, with modernization projects in New York, Toronto, and other metro hubs.

Europe: Mature but investing heavily in upgrading aging systems with a sustainability focus.

Latin America, Africa & Middle East: Emerging hotspots for urban transit, addressing rapid metropolitan growth.

📌 Buy the full report for complete insights: Purchase Report.

Competitive Landscape

Key global players shaping the industry include:

CRRC Corporation Limited – Leader in rolling stock production.

Siemens Mobility – Specialist in automation and signaling.

Alstom SA – Pioneer in integrated metro systems.

Bombardier Transportation (Alstom Group) – Strong in rolling stock and signaling.

Hyundai Rotem Company – Key supplier for Asian markets.

Hitachi Rail & Ansaldo STS – Innovators in automation and signaling.

Kawasaki Heavy Industries – Specialist in advanced rail technology.

Toshiba Corporation & Thales Group – Providers of electronic, signaling, and communication systems.

Conclusion

The metro rail infrastructure market stands at the forefront of global urban transformation. While the sector grapples with financing, land, and regulatory complexities, its long-term prospects remain highly positive. With governments prioritizing sustainable mobility and technology redefining efficiency, metro systems are becoming indispensable to modern urban life.

By 2033, metro rail infrastructure will not only serve as a mobility solution but also as a catalyst for economic growth, environmental sustainability, and enhanced quality of urban living.