According to IMARC Group's report titled "India Machine Tools Market Size, Share, Trends and Forecast by Tool Type, Technology Type, End Use Industry, and Region, 2026-2034", the report offers a comprehensive analysis of the industry, including industry growth, trends, share, and regional insights.

India's machine tools sector is at an inflection point transitioning from import dependency toward indigenous manufacturing leadership, backed by verified PLI investments, accelerating automation adoption, and deepening demand from automotive and aerospace industries. Here is what investors need to know:

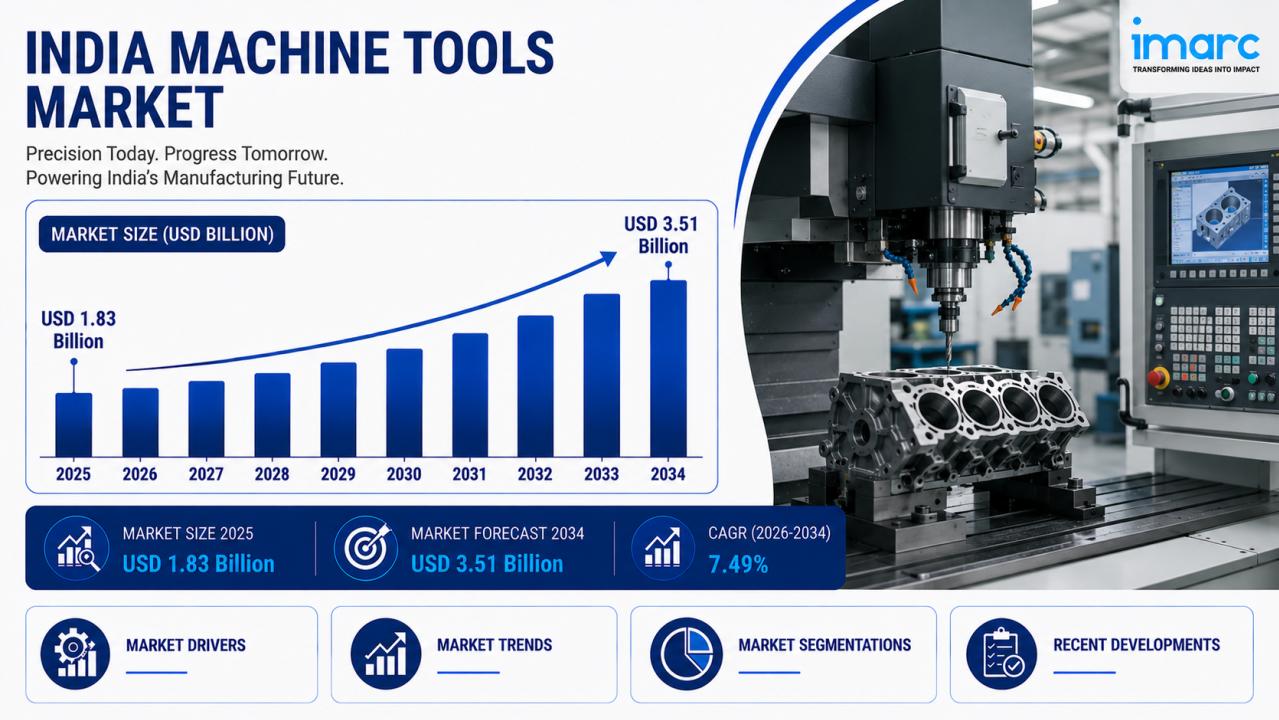

- Market valued at USD 1.83 Billion in 2025, projected to reach USD 3.51 Billion by 2034 at a CAGR of 7.49%.

- Metal cutting leads tool type at 52%; CNC technology dominates at 60%, reflecting India's decisive shift toward precision-driven, Industry 4.0-compatible manufacturing.

- Automotive holds 29% end-use share, with EV production creating additive machining requirements for battery housings and electric motor components.

- North India leads regionally at 30%, anchored by manufacturing clusters across Uttar Pradesh, Haryana, Punjab, and Rajasthan.

- The PLI scheme has attracted nearly ₹2 Lakh Crore in realized investments, establishing the most favorable policy environment the sector has seen.

The Strategic Market Challenge: Navigating the Machine Tools Market in India

The most structurally significant challenge is the fragmented domestic component ecosystem. Critical sub-assemblies precision bearings, linear motion guides, and CNC control systems remain heavily import-dependent, exposing manufacturers to currency volatility and extended lead times. This dependency creates a structural ceiling on cost competitiveness for domestic OEMs and constrains India's ambition to become a globally significant machine tool exporter by 2034. Addressing component localization is the sector's most consequential medium-term priority.

➤ Access Industry-Focused Insights and Future Forecasts - Request Sample Report

India's Strategic Vision for the Machine Tools Market:

- PLI Scheme Verified Disbursement: The government confirmed the PLI scheme has attracted nearly ₹2 Lakh Crore in realized investments, directly incentivizing machine tool manufacturing capacity expansion and import substitution.

- National Capital Goods Policy: Specifically targets reducing machine tool import dependency and developing domestic manufacturing depth across critical capital goods categories.

- Make in India Manufacturing Expansion: In December 2025, Tsugami inaugurated a Rs 300 Crore assembly and foundry facility in Chennai India's first Japanese machine tool foundry directly translating policy intent into foreign capital deployment.

- Industrial Corridor Development: Ongoing investment in manufacturing corridors across North and South India is expanding cluster density, creating concentrated demand nodes for advanced machining equipment.

Why Invest in the India Machine Tools Market: Key Growth Drivers & ROI

- Automotive and EV Production Driving Dual-Track Demand: In July 2025, Tata Motors began production of the Harrier EV at its Pune facility creating additive machining requirements for battery housings and lightweight structures alongside existing ICE component production. Schaeffler India's May 2025 opening of a 16,500 sq. metre facility in Shoolagiri, Tamil Nadu, producing planetary gears and hybrid transmission components further confirms that EV manufacturing is expanding not replacing machine tool demand from automotive OEMs.

- Smart Manufacturing Adoption Delivering Measurable ROI: The 2025 IMTEX Tooltech exhibition hosted 1,100 exhibitors from 23 countries in Bengaluru, showcasing smart machine tools, IoT integration, and digital manufacturing innovations. Siemens India's Sinumerik ONE CNC systems with digital twin integration demonstrated at IMTEX 2025 enable virtual commissioning and high-precision multi-axis machining, delivering documented productivity improvements that make the investment case for CNC upgrades increasingly quantifiable for CFOs.

- Foreign OEM Investment Validating India's Manufacturing Credentials: Brother Machine Tools India's June 2025 opening of an advanced Technology Center in Pune featuring the Speedio CNC series and Made-in-India S700Bd1 reflects how global machine tool OEMs are investing in India-based application demonstration and customer capability-building infrastructure, compressing sales cycles and validating long-term market confidence.

➤ Explore the Complete TOC and Data Coverage - Get Full Brochure

India Machine Tools Market Trends & Future Outlook:

- Hybrid additive-subtractive manufacturing is gaining commercial validation BFW's June 2024 partnership with ADDiTEC integrating Liquid Metal Jetting and Directed Energy Deposition with CNC machining marks a commercially significant proof point for India.

- Sustainability is reshaping equipment procurement priorities CERATIZIT's 2025 IMTEX roadmap targeting 35% CO₂e emission reduction by 2025 and 60% by 2030 signals that green manufacturing compliance is becoming a measurable procurement criterion.

- CNC affordability improvements are accelerating SME adoption, extending precision machining capability into small and medium enterprises seeking competitive advantages previously accessible only to large manufacturers.

- North India's 30% regional dominance is structurally reinforced by automotive cluster expansion in Haryana and Uttar Pradesh, with ongoing logistics infrastructure investment sustaining above-market growth through 2034.

Regulatory Landscape & Policy Catalysts in India:

- PLI Scheme (Nearly ₹2 Lakh Crore Realized): Verified disbursements confirm the scheme is translating into actual manufacturing capacity expansion providing investors with an audited demand signal rather than policy aspiration.

- National Capital Goods Policy: According to the Ministry of Heavy Industries, the policy targets doubling the capital goods sector's GDP contribution and reducing import dependence with machine tools identified as a priority sub-sector.

- Make in India FDI Facilitation: Single-window approvals and FDI facilitation are enabling international OEMs like Tsugami to establish India manufacturing bases building domestic supply chain depth while reducing import exposure.

- Skill Development NSDC Alignment: National Skill Development Corporation programs targeting advanced CNC operation and maintenance are progressively addressing the technical workforce gap that currently limits optimal machine tool performance optimization across manufacturing facilities.

Market Segmentation Breakdown and Share Analysis:

Analysis by Tool Type:

- Metal Cutting (Dominant Segment due to high demand in automotive & aerospace)

- Metal Forming

- Accessories

Metal cutting dominates the market with a 52% share in 2025, driven by extensive usage in automotive component manufacturing, aerospace parts production, and precision engineering applications requiring high accuracy.

Analysis by Technology Type:

- CNC (Computerized Numerical Control) (Fastest growing due to automation trends)

- Conventional

CNC leads the market with a 60% share in 2025, owing to its superior precision, improved operational efficiency, reduced manual intervention, and seamless integration with Industry 4.0-enabled smart manufacturing systems.

Analysis by End Use Industry:

- Automotive (Largest revenue contributor)

- Aerospace and Defense

- Electrical and Electronics

- Consumer Goods

- Precision Engineering

- Others

Automotive represents the largest segment with a 29% market share in 2025, supported by strong demand for machining of engine parts, transmission components, and critical systems for both conventional and electric vehicles.

Regional Insights:

- North India: Major market driver due to strong automotive and engineering clusters in Delhi-NCR, Haryana, and Punjab.

- West and Central India: Key hub for heavy engineering and electronics, led by Maharashtra and Gujarat.

- South India: Prominent for automotive and aerospace manufacturing in Tamil Nadu and Karnataka.

- East India: Emerging center for industrial machinery.

North India holds the leading position with a 30% share in 2025, driven by the presence of major manufacturing hubs, well-established industrial corridors, and robust infrastructure enabling large-scale production growth.

By the IMARC Group, the Top Competitive Landscape & their Positioning:

Covering an in-depth analysis of the competitive landscape, market structure, key player positioning, competitive dashboards, top winning strategies, and detailed profiles of all major industry participants you will gain access to all these exclusive insights within the full research report.

Note: If you need specific information that is not currently within the scope of the report, we can provide it to you as a part of the customization.

➤ Tailor the Research to Your Exact Business Needs - Request Customization

Frequently Asked Questions (FAQs):

Q1: What is the current value and projected growth of the India Machine Tools Market?

According to IMARC Group, the India machine tools market was valued at USD 1.83 Billion in 2025 and is projected to reach USD 3.51 Billion by 2034, growing at a CAGR of 7.49% from 2026 to 2034. Growth is driven by industrialization, PLI-backed manufacturing investment, automotive and EV production expansion, and accelerating CNC and automation adoption.

Q2: Which tool type and technology segments lead the market?

Metal cutting leads tool type at 52%, encompassing turning centers, milling machines, and drilling equipment serving automotive and aerospace fabrication. CNC technology leads at 60%, driven by demand for precise positioning, multi-axis movement capability, and seamless Industry 4.0 integration with adoption accelerating across SMEs as system affordability improves.

Q3: Which end-use industry generates the highest machine tool demand?

Automotive leads at 29%, driven by engine block, transmission, and chassis machining requirements. The EV transition is creating additional demand for battery housing and electric motor component machining making automotive a dual-track demand source that compounds conventional ICE machining volumes with new EV-specific requirements.

Q4: What are the primary challenges constraining market growth?

Three constraints limit velocity: high capital costs creating financing barriers for SMEs; fragmented domestic component ecosystems sustaining import dependency for precision bearings and control systems; and skilled workforce shortages in CNC operation and advanced automation maintenance gaps that current technical education infrastructure has not yet adequately bridged.

Q5: What recent developments signal the market's growth trajectory?

Tsugami's Rs 300 Crore Chennai facility, Brother Machine Tools India's Pune Technology Center, and BFW's additive-CNC hybrid platform partnership collectively demonstrate both domestic investment confidence and international OEM commitment to India's machine tool ecosystem providing investors with multiple, independently verifiable proof points of sustained market momentum.

Strategic Insight & Verdict

India's machine tools market presents a policy-reinforced, technology-driven investment opportunity anchored in automotive EV transition, PLI-backed capacity expansion, and Industry 4.0 adoption. Based on rigorous market analysis, we at IMARC Group have observed that the compounding effect of EV production ramp-up, smart manufacturing adoption, and verified PLI disbursements is creating a demand environment where early, capability-led positioning will generate durable competitive and financial returns through 2034.