Education costs in India are rising faster than inflation, making it essential for parents to start planning early. Whether you're dreaming of sending your child to IIT, a top medical college, or an international university, having a solid financial plan ensures their aspirations don't become financial burdens.

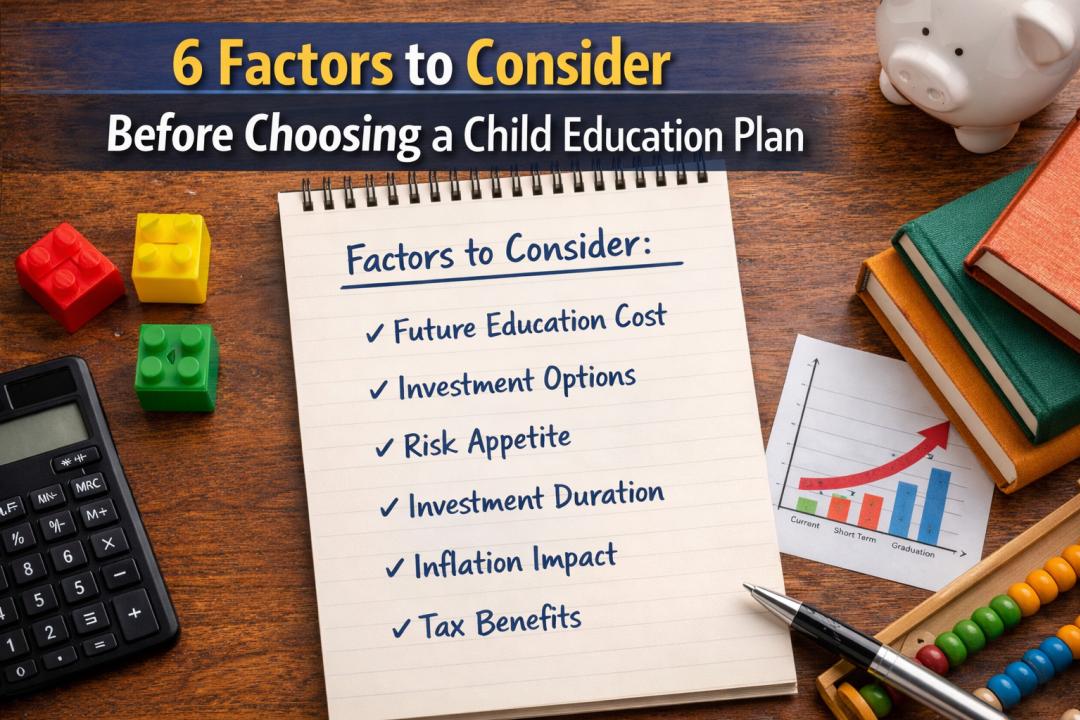

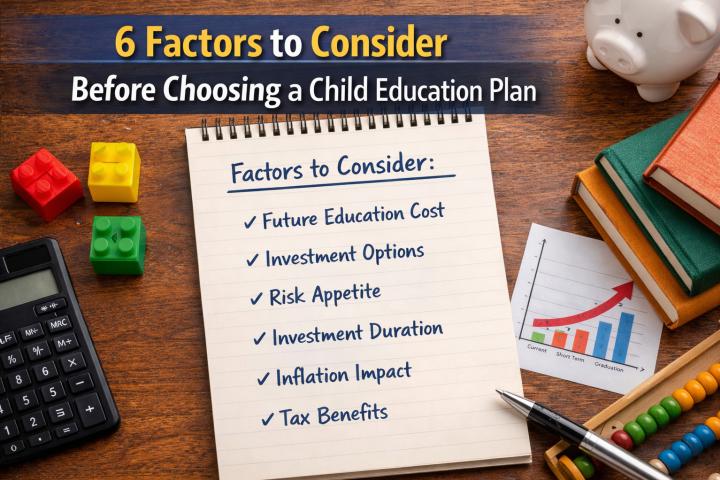

A child education savings plan is more than just a savings account. It's a strategic investment approach designed to accumulate sufficient funds over time to meet your child's educational needs. With tuition fees for professional courses now ranging from lakhs to crores, choosing the right savings plan can make all the difference. In this comprehensive guide, we'll explore six critical factors you must consider before selecting a child education savings plan that aligns with your goals.

1. Time Horizon Until Your Child Needs the Funds

The number of years you have before your child enters higher education is perhaps the most crucial factor. If your child is just born, you have 18 years to build a corpus. If they're already 10, you have only 8 years.

Longer time horizons allow you to take advantage of equity investments, which historically deliver higher returns despite short term volatility. For periods exceeding 10 years, equity mutual funds have consistently outperformed traditional savings instruments. The power of compounding works best when given time, turning even modest monthly investments into substantial amounts.

Shorter time horizons require more conservative approaches. If your child is already in their teens, you might need to balance equity exposure with debt instruments to protect accumulated capital from market volatility. Understanding your timeline helps you choose between aggressive growth strategies and capital preservation approaches.

2. Estimated Education Costs and Inflation Impact

Calculating how much you'll actually need is essential. A bachelor's degree in engineering that costs 10 lakhs today might cost 25 lakhs in 15 years due to education inflation, which typically runs higher than general inflation.

Research current costs for the type of education you're planning for, whether it's undergraduate programs, postgraduate studies, or international education. Then factor in an annual inflation rate of 8 to 10 percent to estimate future costs. This realistic projection helps you set appropriate investment targets.

Tools like a mutual fund return calculator can help you determine how much you need to invest monthly to reach your target corpus. By inputting your time horizon, expected returns, and target amount, you can create a realistic savings roadmap that accounts for inflation and compound growth.

3. Risk Tolerance and Investment Mix

Every parent has different comfort levels with investment risk. Some are willing to accept market volatility for potentially higher returns, while others prefer guaranteed returns even if they're lower.

Your risk tolerance should guide your asset allocation between equity and debt. Equity investments offer higher growth potential but come with market risk. Debt instruments provide stability but might not beat inflation over long periods. A balanced approach often works best, with higher equity allocation for longer horizons and gradual shift toward debt as the target date approaches.

Understanding the benefits of mutual funds helps you make informed allocation decisions. Mutual funds offer professional management, diversification, liquidity, and tax efficiency, making them excellent vehicles for education planning. Equity mutual funds can deliver inflation beating returns over 10 plus year periods, while debt funds provide stability for shorter horizons.

4. Flexibility and Liquidity Requirements

Life is unpredictable. Your child might need funds earlier than planned, or you might face financial emergencies requiring access to your savings. Therefore, flexibility and liquidity are crucial considerations.

Some education plans lock your money for fixed periods with penalties for early withdrawal. Others, like mutual funds, offer better liquidity, allowing you to redeem investments when needed. Systematic Investment Plans (SIPs) in mutual funds provide flexibility to increase, decrease, or pause contributions based on your financial situation.

Consider plans that don't penalize you for accessing your money. While discipline is important, rigid lock in periods can create problems during emergencies. Balance commitment with the flexibility to adapt as circumstances change.

5. Tax Efficiency and Benefits

Tax treatment significantly impacts your effective returns. Investments that offer tax deductions or tax free growth can substantially boost your final corpus.

Equity Linked Savings Schemes (ELSS) provide tax deductions under Section 80C while investing in equity markets. Public Provident Fund (PPF) offers tax free returns but with lower growth potential. Sukanya Samriddhi Yojana provides excellent benefits specifically for girl children. Understanding these tax implications helps you choose more efficient investment vehicles.

Long term capital gains from equity mutual funds held over one year currently enjoy favorable tax treatment compared to other investment options. Factor in post tax returns when comparing different education savings plans to get a true picture of wealth accumulation.

6. Insurance Coverage and Risk Protection

What happens to your child's education plans if something happens to you? This uncomfortable but essential question highlights the need for insurance coverage within your education plan.

Some child education plans come bundled with life insurance, ensuring the plan continues even if the parent passes away. While these combination products offer peace of mind, they often deliver lower investment returns compared to buying term insurance separately and investing the difference in higher yielding instruments.

Consider a strategy where you maintain adequate term life insurance coverage alongside your investments. This separation often proves more cost effective while providing better returns and comprehensive protection. The insurance component ensures your child's education remains funded regardless of unforeseen circumstances.

How Quant Trade Supports Your Education Planning

Making informed investment decisions for your child's future requires access to comprehensive data and analytical tools. Quant Trade offers powerful platforms designed to help Indian parents make data driven choices for education planning.

With features that allow you to analyze mutual fund performance, compare returns across categories, evaluate risk metrics, and project future values, you get everything needed to build an effective education corpus. The platform's quantitative research approach removes guesswork from fund selection, helping you identify schemes that align with your goals, timeline, and risk tolerance.

Secure Your Child's Educational Future Today

Your child's dreams deserve a solid financial foundation. Don't leave their education to chance or last minute scrambling. Visit Quant Trade now to access powerful investment tools, comprehensive fund analysis, and expert guidance tailored for education planning. Our data driven platform helps you select the right mutual funds, track performance, and stay on course to meet your goals.

Frequently Asked Questions

Q1: When should I start a child education savings plan?

The best time is as soon as possible, ideally at birth or within the first few years. Starting early gives you the longest time horizon, allowing even small monthly investments to grow substantially through compounding.

Q2: How much should I invest monthly for my child's education?

This depends on your target corpus, time horizon, and expected returns. Use a mutual fund calculator to determine monthly investment amounts. For example, to accumulate 50 lakhs in 15 years at 12% annual returns, you'd need to invest approximately 12,000 rupees monthly.

Q3: Are mutual funds better than traditional insurance based education plans?

Mutual funds typically offer higher return potential and better flexibility. Insurance based plans provide guaranteed benefits but often with lower returns. Many experts recommend separating insurance and investment for better overall outcomes.

Q4: Should I choose equity or debt funds for education planning?

For time horizons over 10 years, equity funds generally deliver better inflation adjusted returns. As the target date approaches, gradually shift to debt funds to protect accumulated capital. A balanced approach works best for most parents.

Q5: Can I withdraw from my child education plan in case of emergency?

This depends on the plan type. Mutual funds offer good liquidity with redemption possible within a few days. Some insurance based plans have lock in periods with surrender charges. Always check liquidity terms before investing.