LCD Panel Market Research Report

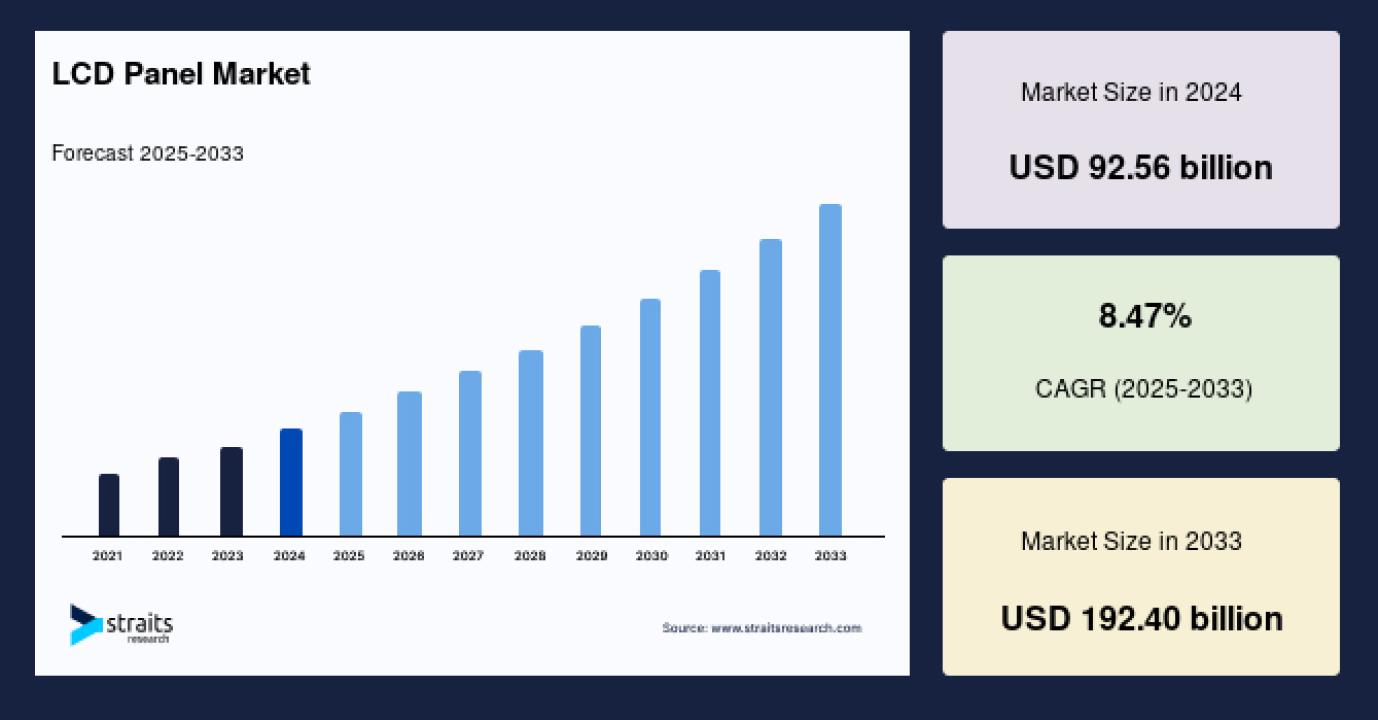

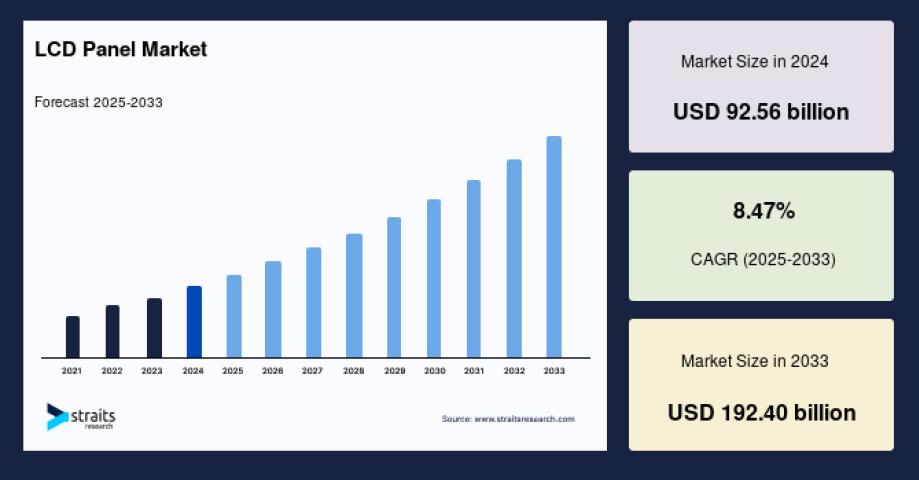

The global LCD panel market is experiencing robust growth driven by rising demand for consumer electronics, digital transformation across industries, and technological advancements in display quality. Valued at USD 92.56 billion in 2024, the market is projected to grow from USD 100.40 billion in 2025 to reach USD 192.40 billion by 2033, exhibiting a CAGR of 8.47% during the forecast period.

For comprehensive market insights and detailed analysis, access the full report at https://straitsresearch.com/report/lcd-panel-market/request-sample.

Market Drivers

The LCD panel market is propelled by several key factors. Rising demand from education and corporate sectors due to increased digitalization and remote operations is a major driver, as educational institutions integrate LCD panels into smart classrooms and e-learning platforms, especially in emerging economies. Corporate sectors are utilizing LCD screens for video conferencing, digital signage, and collaborative tools to improve productivity.

The growing incorporation of LCD panels in automobiles is driving significant demand, with modern vehicles, especially electric and connected cars, featuring advanced infotainment systems and digital instrument clusters powered by LCDs. The increasing use of LCD displays in public infrastructure projects, including smart city initiatives, further strengthens market growth, as these panels are widely adopted in digital billboards, transport information systems, and surveillance displays.

Growing demand for consumer electronics continues to be a key driver, as digital life>

Market Challenges

Despite robust growth prospects, the market faces significant obstacles. Intense competition from emerging display technologies such as OLED and MicroLED poses the most substantial challenge, as these advanced alternatives offer superior image quality, including deeper blacks, higher contrast ratios, faster response times, and thinner, more flexible form factors.

OLEDs are increasingly being adopted in premium smartphones, high-end televisions, and wearables, while MicroLEDs are gaining traction in large-format displays and next-generation screens. As consumer preferences shift toward more vibrant and energy-efficient displays, LCD panels face challenges in maintaining market share, with many manufacturers reallocating investments toward these next-generation technologies, limiting further innovation and cost reduction in LCDs.

Impact of War on Current Market: Geopolitical tensions and regional conflicts have created both challenges and opportunities in the LCD panel market. Military conflicts drive increased defense spending on surveillance systems and digital displays for military applications, boosting demand for ruggedized LCD panels. However, supply chain disruptions, raw material shortages particularly affecting semiconductor components, and trade restrictions can impact manufacturing operations and increase production costs across the global LCD supply chain.

Market Segments

According to Straits Research analysis, the market is segmented across multiple dimensions:

By Technology Type:

Twisted Nematic (TN) LCD (holds significant share due to low production costs and fast response times)

In-Plane Switching (IPS)

Vertical Alignment (VA)

By Size:

Up to 10 Inches (driven by widespread use in smartphones, tablets, and portable devices)

10-20 Inches

20-40 Inches

Above 40 Inches

By Type:

Rigid LCD Panel (dominates due to durability and cost-effectiveness)

Flexible LCD Panel

By Resolution:

Full HD (1080p) - maintains strong market relevance due to balance of performance and affordability

4K and 8K

By Application:

Consumer Electronics (key driver fueled by high demand for televisions, smartphones, tablets, and monitors)

Automotive

Healthcare

Industrial

The twisted nematic (TN) LCD segment holds a significant share due to its low production costs and fast response times, making it ideal for gaming monitors and budget-friendly displays. The consumer electronics segment is a key driver, fueled by high demand for televisions, smartphones, tablets, and monitors, with rapid technological advancements and rising disposable incomes supporting strong LCD integration in these devices.

Regional Analysis

Asia Pacific remains the dominant production and consumption hub for LCD panels, supported by a robust consumer electronics manufacturing base and increasing urbanization. The region leads in TV, smartphone, and monitor shipments, prompting continuous innovation in panel technology, including higher refresh rates and ultra-slim designs. China's LCD panel market dominates global production, driven by major players like BOE Technology and TCL CSOT, with government subsidies and massive investments in Gen 10.5+ fabs enhancing domestic manufacturing capacity.

North America represents the fastest-growing market, witnessing stable growth driven by high adoption of advanced consumer electronics and growing demand for large-screen televisions and gaming monitors. The region's tech-savvy population, along with strong entertainment and media consumption trends, supports continued investment in 4K and smart displays. The United States LCD panel market benefits from high consumer demand for smart TVs, laptops, and automotive displays, with the expansion of EVs driving LCD adoption in infotainment systems.

Europe benefits from growing industrial and healthcare applications, including advanced display systems for monitoring and diagnostics. High environmental regulations are pushing manufacturers toward sustainable, energy-efficient LCD solutions. Germany's LCD panel market benefits from the nation's automotive leadership, as BMW, Mercedes-Benz, and Volkswagen upscale 10-inch-plus infotainment LCDs and instrument clusters for new EV lines.

Top Players Analysis

The LCD panel market features several key players implementing diverse strategies. Major companies include Samsung Display Co., Ltd., LG Display Co., Ltd., AU Optronics Corp., BOE Technology Group Co., Ltd., and Innolux Corporation.

Samsung Display Co., Ltd. maintains market leadership through continuous innovation in display technology and massive production capacity across multiple manufacturing facilities globally. The company focuses on developing advanced LCD technologies while transitioning toward next-generation display solutions.

LG Display Co., Ltd. is a leading South Korean manufacturer of thin-film transistor liquid crystal display (TFT-LCD) panels and organic light-emitting diode (OLED) panels. The company supplies high-resolution panels for televisions, monitors, laptops, smartphones, and automotive displays, operating manufacturing plants in South Korea, China, and Vietnam.

BOE Technology Group Co., Ltd. dominates China's LCD panel production with massive manufacturing capacity, having exceeded 60 million LCD units output in 2023. The company benefits from significant government support and investments in advanced manufacturing facilities.

These companies are focusing on expanding production capacity, enhancing panel resolution and energy efficiency, adopting cost-effective manufacturing techniques, and investing in R&D to develop thinner, flexible, and ultra-high-definition panels.

Market Outlook

The LCD panel market is positioned for sustained growth, driven by ongoing technological advancements aimed at enhancing performance, display quality, and energy efficiency. Despite competition from emerging display technologies, the market remains resilient due to continuous innovation in manufacturing processes and diverse applications across industries from consumer electronics to automotive and healthcare sectors.

Purchase the complete study at https://straitsresearch.com/buy-now/lcd-panel-market.

Frequently Asked Questions

How big is the LCD panel market?

The global LCD panel market was valued at USD 92.56 billion in 2024 and is projected to reach USD 192.40 billion by 2033, growing at 8.47% CAGR during the forecast period.

What drives LCD panel market growth?

Key drivers include rising demand from education and corporate sectors, growing incorporation in automobiles, increasing use in smart city infrastructure, and continued demand for consumer electronics like smartphones, TVs, and tablets.

Which region dominates the LCD panel market?

Asia Pacific is the largest market, led by China's dominant production capacity, while North America is the fastest-growing region due to high adoption of advanced consumer electronics and gaming monitors.

What challenges face the LCD panel industry?

The main challenge is intense competition from emerging display technologies like OLED and MicroLED, which offer superior image quality, higher contrast ratios, and more flexible form factors.

Who are the key players in the LCD panel market?

Major companies include Samsung Display Co., Ltd., LG Display Co., Ltd., AU Optronics Corp., BOE Technology Group Co., Ltd., and Innolux Corporation, focusing on production capacity expansion and technological innovation.